MARKET UPDATE

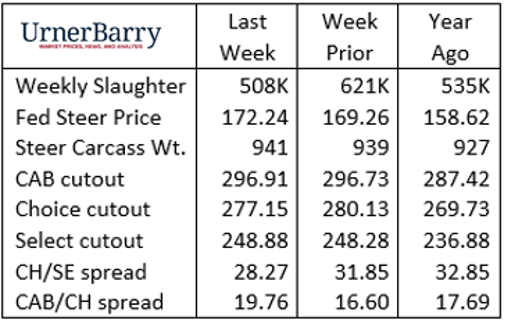

Last week’s holiday-disrupted cattle harvest schedule proved to yield a very small total for the week with an estimated 508,000 head, down 5.6% on the same week a year ago. That suggests packers will need to fill their inventory due to this week’s shortened slaughter from Monday’s holiday.

Further evidence of spotmarket, fed cattle demand came through in a sharp uptick in fed cattle values. Last week’s fed steer price average of $172.24/cwt. was $2.98/cwt. higher than the week prior. The last week of the year often culminates in a brief, bullish fed cattle market and last week’s action adds confirmation to the trend.

Live cattle futures this Tuesday were also much higher as February becomes the front month on the CME board. The February contract was higher by more than $3.25/cwt. by mid-afternoon with April more than $2.00/cwt. higher. Given the recent depression in spot market fed cattle prices it appears to many market observers that a short-term bottom has been marked after a seven-week spiral dropping spot market values $16/cwt.

Carcass cutout values were mixed in last week’s report in what could be summarized as a sideways market. CAB tenderloin prices are rapidly retreating from their lofty record-highs with last week’s $17.40/lb. wholesale price down 7% from the high in late November. Ribeye prices were also a bit lower last week but have only adjusted 2% from their December highs.

Many of the end meat cuts pulled to dramatically lower prices in December as is the seasonal tendency. Last week’s summary showed price stabilizing or slightly higher with the expectation for modestly firmer values in January. Consumer demand following the holidays tends to favor roasts as winter weather develops just as holiday spending hits home for many households with additional buildup of consumer credit card debt.

Carcass Quality Set to Climb Seasonally

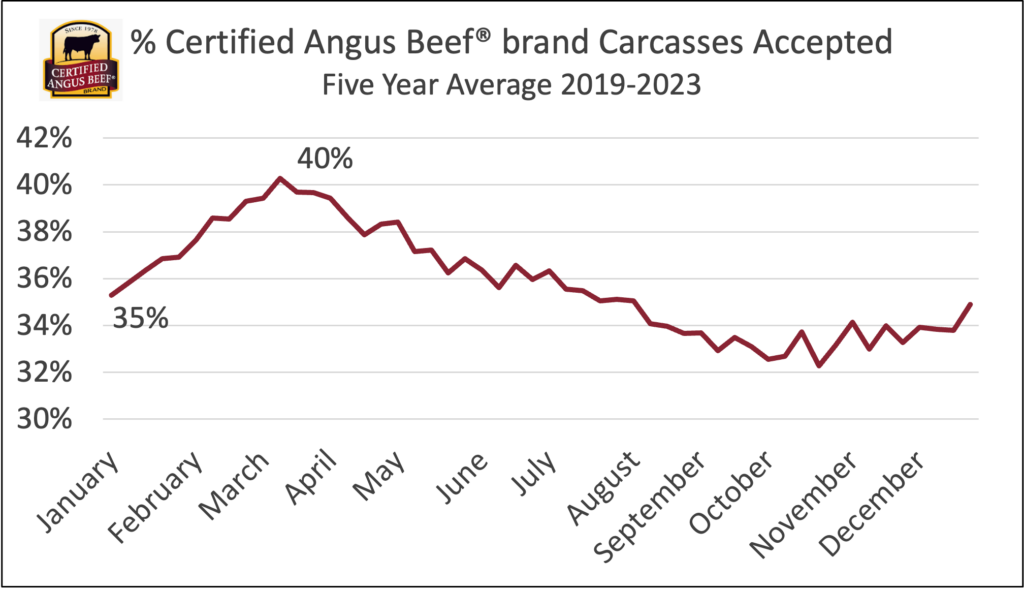

With the arrival of the new year the beef market will rapidly adjust to changes in consumer buying habits. This will remove demand pressure from ribs and tenderloins, realigning the contribution of these most valuable beef cuts to a smaller percentage of carcass value. This expected shift seasonally tends to combine with rising carcass quality grade trends through March, narrowing price spreads between USDA quality grades and CAB branded product.

In the past 5 years the Choice/Select spread has peaked at an average of $22/cwt. in early November, remaining in a range between $20 and $25/cwt. through the first week in December. This November/December timeline has defined the annual widest Choice/Select spread in the average 5-year data, although brief departures to even wider spreads can be noted in other months in given years. The largest CAB cutout premium over USDA Choice followed a similar fourth quarter high in 2022 but has been more common in the low supply/high demand period of early June in other recent years.

The first quarter of 2024 promises to deliver higher average carcass quality grades, particularly as carcass weights remain record-large. The latest confirmed data places steer carcasses at 941 lb. for the week of December 11th, the record so far. The slowed pace of slaughter has yet to show any sustained increases as well. Unless this changes front-end cattle supplies will continue to be elevated along with average days on feed.

These factors should couple with the typical seasonal pattern in the first quarter to track carcass quality to their highest annual levels by March. In March of 2023 CAB carcass certification topped out at 41% of eligible cattle, very near the record of 41.5% set in the same month of 2021. While we won’t predict another record-high this year, the above trends are, so far, aligned to position the share of quality carcasses near the top of the historical range by the end of Q1.

Read More CAB Insider

Carcass Quality Spreads Pop

High quality steak and roast items such as ribeyes, strip loins, tenderloins and sirloins carry an outsized share of the load when it comes to generating pricing separation up and down the carcass quality spectrum.

Chuck and Round Cutout Contribution Increases

In the past two years the chuck and round carcass primals have edged their way upward relative to their contribution to total carcass value. One of the primary reasons for this is the decline in domestic supply of lean grinding beef from cull cows.

CAB Drives Brand Relevance with Specification Update

Evolution of cattle type, management technology and production economics continue to shape the beef business. As a pioneer in the branded beef space, the Certified Angus Beef ® brand has remained relevant throughout the supply chain via continued innovation. Effective the first week of March, the brand will modify its ribeye area (REA) specification from the current 10 to 16 square inch acceptable range to include carcasses wth ribeyes measuring up to 17 square inches.